Have you ever wondered what the difference is between a redraw facility and an offset account — and which one could save you more on your home loan?

It’s a question we get asked all the time, and the answer can make a big difference to how you structure your finances.

Redraw and offset both help reduce the interest you pay, but they’re designed for different types of borrowers.

A redraw facility lets you access any extra repayments you’ve made directly into your home loan. Because the money sits inside the loan, it reduces your loan balance and interest immediately. It’s simple, effective, and great for borrowers who don’t need frequent access to their surplus funds.

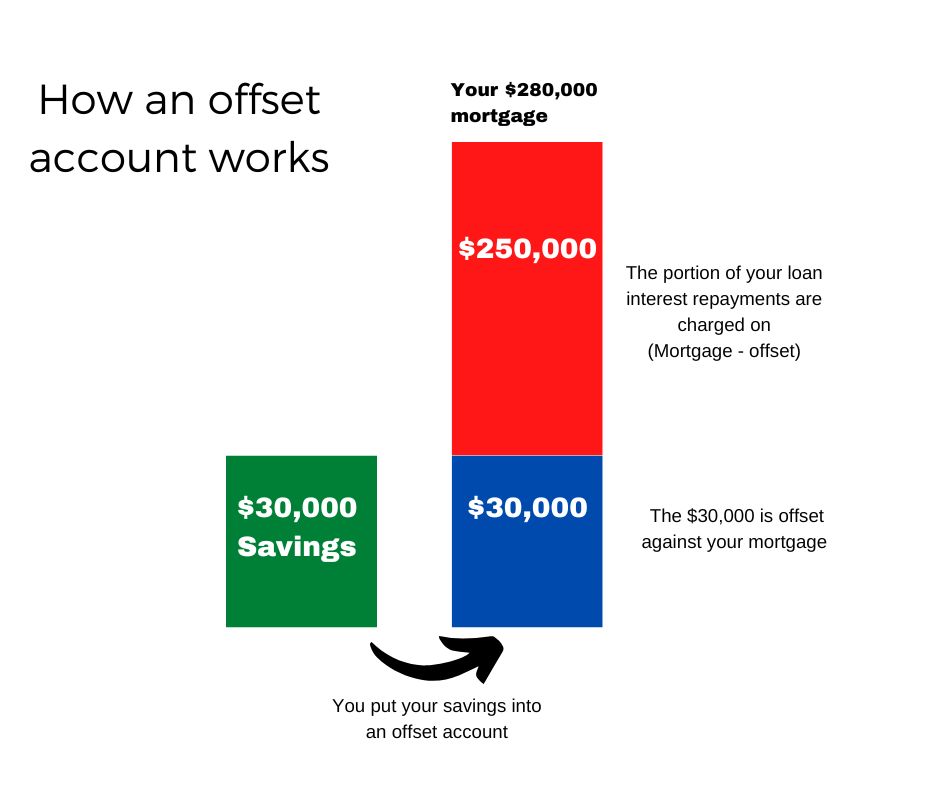

An offset account, on the other hand, works like a regular everyday bank account — but every dollar you keep in it offsets your loan balance for interest purposes. This gives you full flexibility, faster access to your cash, and more control over your savings or emergency buffers.